Hanging in the Balance

Considerable progress was made during the talks with the IMF mission on policy measures to address the domestic and external imbalances

Ishaq Dar

Finance minister

Advertisement

The heroics of Dar backfired. Freezing of exchange rate resulted in a decline in remittances by $1.5 billion and because of the fear of default, the foreign banks did not rollover the deposits of $2.3 billion

Miftah Ismail

Former finance minister

Pakistan manages to get MEFP related to the ninth review of a $7b loan programme

Islamabad: The Pakistan government has somehow managed to salvage some pride by convincing the International Monetary Fund (IMF) to issue the Memorandum of Economic and Financial Policies (MEFP), which is a key document that describes all the conditions, steps and policy measures on the basis of which the two sides declare the staff-level agreement.

Advertisement

After 10 days of intense and one the most difficult discussions, Finance Minister Ishaq Dar told newsmen that the government had received MEFP related to the ninth review of a $7 billion loan programme, indicating that a staff-level agreement with the lender was still pending.

The finance minister made this announcement after the IMF issued a brief statement, which left many questions unanswered and unclear the ambiguity that whether the programme is on the right track or the IMF has been satisfied with the assurances given by the government to meet the conditions prerequisite for the completion of this programme.

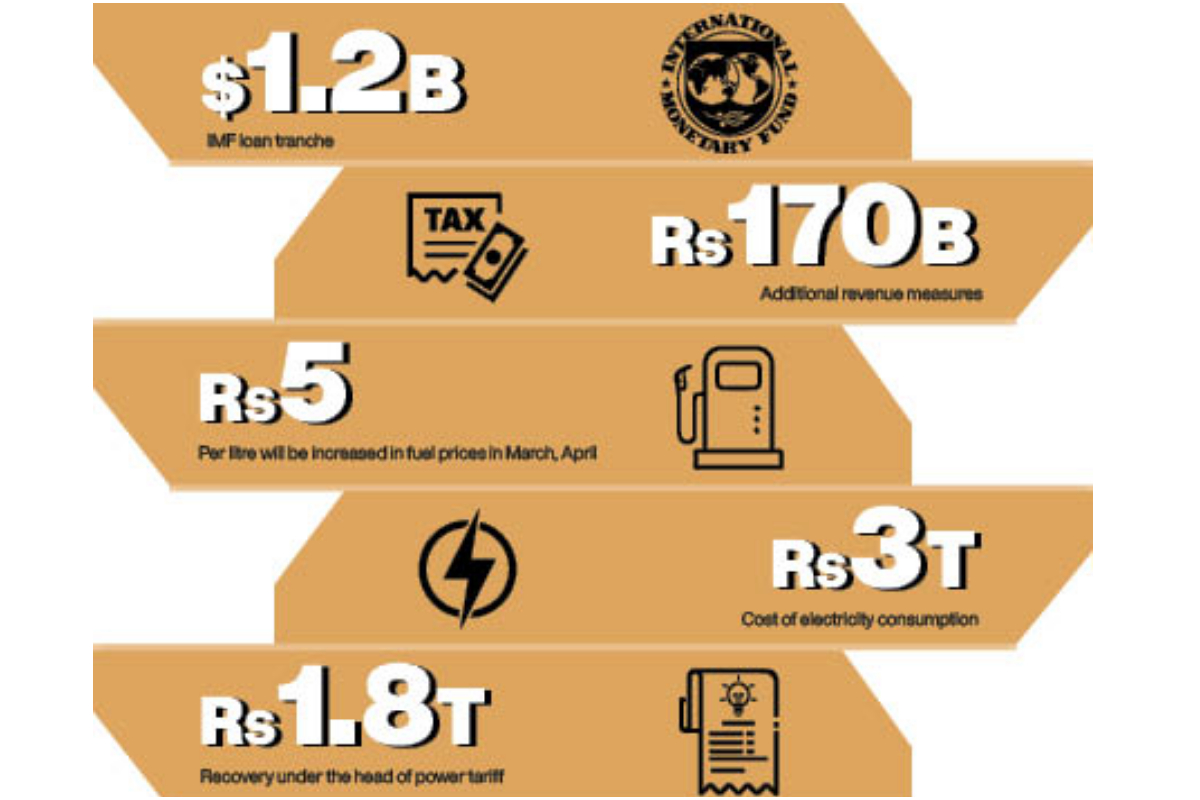

According to Dar, after the successful completion of the ninth review, Pakistan will be entitled to a loan of $1.2 billion.

The IMF team led by its Mission Chief Nathan Porter in a statement said: “The IMF welcomes the prime minister’s commitment to implement the policies needed to safeguard the macroeconomic stability and thanks the authorities for constructive discussions.”

“Considerable progress was made during the talks with the IMF mission on policy measures to address the domestic and external imbalances. The key priorities included strengthening the fiscal position with permanent revenue measures and reduction in untargeted subsidies, while scaling up social protection to help the most vulnerable and those affected by the floods; allowing the exchange rate to be market determined to gradually eliminate the foreign exchange shortage; and enhancing the energy provision by preventing further accumulation of the circular debt and ensuring the viability of the energy sector.”

“The timely and decisive implementation of these policies along with the resolute financial support from the official partners are critical to Pakistan to successfully regain macroeconomic stability and advance its sustainable development,” it added.

Advertisement

“Virtual discussions will continue in the coming days to finalise the implementation details of these policies.”

While elaborating the outcome of the talks, the finance minister said: “Prime Minister Shehbaz Sharif has assured the IMF that the government will honour all its commitments, while the fund has also mentioned this in their statement.”

“Along with the MEFP, the letter of intent (LoI) was also issued, and now, we will go through it and in the next few days, we will hold a virtual meeting with the IMF authorities,” he added.

The government has committed additional revenue measures of Rs170 billion to the IMF, he said and dispelled the impression that taxes of Rs600 to Rs800 billion would be imposed.

However, to a query, he said, this additional revenue of Rs170 billion would be recovered in the remaining four-and-a-half months of this ongoing financial year. The government had already imposed a petroleum development levy of Rs50/litre on petrol and high-speed diesel, while another Rs5/litre will be added in March and April to make it Rs55/litre.

However, the government has outright refused to impose the general sales tax (GST) on petroleum products because it will become too much for the common man, Dar remarked.

Advertisement

The finance minister acknowledged that reforms in certain sectors required by the IMF were in Pakistan’s interest. He criticised the previous Pakistan Tehreek-e-Insaf (PTI)-led government for “economic destruction and misgovernance”.

“In the last five years, our economy has downgraded from 24 to 47 because of wrong policies,” he claimed.

“It is necessary to fix those things,” he said, adding: “These reforms are painful but necessary.”

In the power sector, the electricity consumption costs us Rs3 trillion, whereas the recovery is Rs1.8 trillion and despite providing subsidies of over Rs550 billion, the shortfall is Rs650 billion, which is the root cause of the circular debt.

The government has to increase the electricity tariff but it will continue to subsidise the consumers’ of up to 300 units of electricity, Dar said, adding that the government has committed to the IMF that the gas sector losses would be brought to zero.

Regarding depletion of the foreign exchange reserves to an alarming level of $2.9 billion, he said, the State Bank of Pakistan (SBP) is closely monitoring the situation and discussions were already going on with the multilateral and bilateral donors to build the foreign exchange reserves.

Advertisement

“Our friendly countries had already publicly said that once the IMF programme will be back on track, they will extend the loans,” he remarked.

“In 1999 after the nuclear tests, our foreign exchange reserves were less than $500 million, but even then, we did not default, so let me assure you that nothing such will happen.”

Once the government gets enough funding from the donors all the letters of credit (LCs) would be cleared, the finance minister noted.

“The government has agreed to increase the allocation for the Benazir Income Support Programme (BISP) to Rs400 billion from Rs360 billion to help the most vulnerable people hit by inflation.”

For Dar, there was a credibility gap, as the IMF did not trust the government because of the PTI government’s actions.

“They say not only the previous government failed to implement the agreement but also reversed when the vote of no-confidence was brought [against Prime Minister Imran Khan]. “The negotiations were hard but we agreed only to what was doable,” he said.

Advertisement

Regarding privatisation of the state-owned enterprises (SoEs), the finance minister said discussions for the privatisation of power plants of Haveli Bahadur Shah and Baloki were already in advance stage.

Former finance minister Miftah Ismail said that a delay in increasing the gas and electricity tariffs and reducing the petroleum prices cost dearly to the nation.

“Now, it becomes obvious that the heroics of Dar backfired. According to him, freezing of the exchange rate resulted in a decline in remittances by $1.5 billion and because of the fear of default, the foreign banks did not rollover the deposits of $2.3 billion.

If Dar has taken the measures by now, the reserves of the State Bank could easily stand at $8 to $9 billion and the country might not face the default risk.

For him, the unfunded subsidy of Rs100 billion to the textile sector has irked the IMF and now the government might have to withdraw it to keep the IMF programme intact.

Even after reaching the staff-level agreement, the IMF Board will approve the tranche of $1.2 billion after getting the assurance from friendly countries such as Saudi Arabia or other countries to finance the shortfall of $4 billion.

Advertisement

Pakistan’s debt servicing requirement now reaches $20 billion annually and this could only be met by increasing exports.

Advertisement

Catch all the Economic Pulse News, Breaking News Event and Latest News Updates on The BOL News

Download The BOL News App to get the Daily News Update & Live News.

End of Article

More Newspaper Articles

Advertisement

Read the complete story text.

Read the complete story text. Listen to audio of the story.

Listen to audio of the story.